By Jim Flammang

Paying cash for your next car? Don’t laugh. Quite a few families and individuals do, shunning the entire financing process. In fact, the number of shoppers who finance their vehicle has been declining.

How to Finance Your Car

According to Melinda Zabritski, senior director of Automotive Financial Solutions at credit reporting company Experian, 81.2 percent of new vehicles were being financed as of early 2021 (down from 87 percent). Used cars are far less likely to be purchased with time payments: only about 34.5 percent, versus nearly 43 percent in 2020. Before the COVID pandemic arrived, well over half of used vehicles were financed.

In the early days of motoring, buyers typically paid cash. Only the well-off qualified for credit of any kind. Installment plans gradually began to emerge in the 1920s and ’30s, but didn’t become common until after World War II. During the postwar economic boom, credit purchases helped usher in the consumer society, centering on “easy” payments – which were seldom all that easy, for most families.

What’s New About Auto Loans?

Financing, like the overall car-buying process, is changing: mainly, going digital, as technology keeps boring its way into the automobile business. Computerization might be at the core of today’s installment payment system, but the principles are largely unaltered.

What you have to pay, ultimately, is still a combination of down payment (possibly including a trade-in) and total monthly payments. The size of the latter is determined by interest rate (APR – Annual Percentage Rate), the amount to be financed, and the loan term (duration).

As they have for decades, many shoppers practically ignore the total amount to be paid over a loan term. They’re most concerned about the monthly payment, hoping to keep it as low as possible. As a result, they pay plenty in interest.

Several factors affect the details of an auto loan. Your credit score tops the list, along with your credit history (including its duration), employment, income, and whether you own or rent your residence.

If a credit grantor is dissatisfied with some facts and figures in your loan application, you’re likely to be charged a higher APR, resulting in bigger payments each month. You might have to come up with a larger down payment. Or, if you’re judged un-creditworthy, your application could be rejected completely. Nowadays, the decisions might be made by a computer algorithm rather than a human, but the result is essentially the same.

Should I Buy a Car From CarMax?

Credit Scores

Twin factors, Credit Score (a three-digit figure) and Credit Status, are the primary way to categorize potential loan customers.

Most often called FICO scores, because they’re calculated by the Fair Isaac Corporation, these numeric gateways to the credit world are issued by three separate credit bureaus: Experian, Equifax, and TransUnion. Each organization has its own method of gathering data and using it to assess a person’s creditworthiness, coming up with a score that nearly always differs a bit from the other two.

Credit Status

Credit bureaus place loan applicants into one of five categories, based upon their three-digit credit score: Super Prime, Prime, Nonprime, Subprime, and Deep Subprime. As you can imagine, those with a Super Prime rating are the most likely to get a loan with a low interest rate, while credit-troubled Deep Subprime applicants are sure to get the least favorable terms – if they’re granted credit at all.

FICO scores from Experian, for instance, range from 300 to 850:

- Super Prime (781-850)

- Prime (661-780)

- Nonprime (601-660)

- Subprime (501-600)

- Deep Subprime (300-500)

Credit Karma suggests that five basic elements enter into the calculation of a person’s credit score. Payment history accounts for 35 percent of the decision, amount owed 30 percent, and length of credit history 15 percent. Amount of new credit and the credit mix are worth 10 percent each.

Customers who fall into the Prime or Super Prime category account for 65 percent of total financing, according to Experian. Nonprime applicants (with FICO scores below 601) make up just 35 percent.

Whether human or digital, financing decision-makers typically take these five categories as gospel. Unless some tangible credit-related action warrants raising one’s score (or lowering it), the FICO score remains firm. Establish a clean record of on-time payments, and you may be rewarded with a higher score, allowing access to more favorable loan terms.

Amount Financed

After all fees or charges are added to the price of the car you’re buying, the total figure is the amount to be financed. Experian reported early in 2021 that the average amount financed on new cars was $35,392, versus $33,833 in the previous year. For used cars, the average was $22,375 (increased from $20,689).

Down Payment

One of the best ways to keep from spending too much on interest is to present a sizable down payment. Obviously, not everyone can follow this sensible advice.

If you’re trading in your old car, the agreed-upon price for that oldie is applied to the down payment. A higher trade-in value translates to a reduced initial payment.

If your current car isn’t paid for, trading it in can get tricky, and might not help much to sway a loan grantor’s decision. Whenever you owe more on a vehicle than it’s currently worth, you’re in a state of “negative equity.” Or, in more straightforward terms, you’re “upside down.” Postponing the purchase until you’ve paid for the old car, or at least come closer to the end of its term, might be wiser.

Low down payments have been the rule lately. But in the past, 20 percent or more was common for new-car purchases. Edmunds reported in 2019 that the average was 11.7 percent. Kelley Blue Book, among others, recommends at least 10 percent down.

Car Shopping Tips: Test Drive Checklist

APR (Interest Rate)

APR (Interest Rate)

Vehicle supply is one factor in assessing interest rates. Super-low rates aren’t as likely when supply is low and selling prices (consequently) are high. That’s what happened early in 2021, as the pandemic began to ease. Credit-grantors of any stripe don’t feel obligated to offer a low APR, any more than a low car price, when demand is so high.

Experian’s first-quarter 2021 report found that APRs for new cars averaged 4.1 percent (down from 5.2 percent in 2020). Used car APRs averaged 8.7 percent.

Zero-interest loans may be especially tempting, but beware. The no-interest promotion may apply only to the first segment of the loan term; then, the rate shoots up. No-interest might be valid only for shorter-term loans, with higher monthly payments.

Loan Term (Duration)

Short-term loans (24- or 36-month) used to be fairly common, but for years the trend has leaned heavily toward long-term durations: 60-, 72-, or even 84-month. Some 96-month contracts might even turn up, but the average new-vehicle term is 69.5 months. as reported in Experian’s first-quarter 2021 survey. For used vehicles, the average reached a record high at 65.7 months.

Monthly Payments

Experian reports that the average monthly payment for new-car loans on new vehicles was $577, as of early 2021. For used cars, it’s a more tolerable $412, but even that figure is beyond the means of many shoppers. Unless you come up with a more sizable down payment – or choose a cheaper vehicle – nothing is likely to reduce that every-month figure. Leasing may require a lower monthly outlay, but that’s typically available only to customers with a strong credit rating.

Not So Complicated: It’s All Basic Math

Like filling out income tax forms, loan contracts make many customers uneasy. They’re intimidated by all the numbers floating on the contract page.

Auto contracts are actually nothing more than basic math – with a garble of fine print appended to the bottom. The only figures that really matter are the purchase price of the car, the amount to be financed, and the specific elements: APR, term, down payment, and monthly payment. Nothing more than a simple electronic calculator – or the ability to do basic arithmetic by hand – should be needed. Stay calm, and don’t let yourself be rushed.

In theory, at least, the interest rate (APR) and loan term are negotiable. Don’t expect miracles, though. Neither the dealership’s F&I (Finance and Insurance) person nor the equivalent decider at a bank or credit union is obligated to make any change at all, much less a substantial one. Some remain immovably firm.

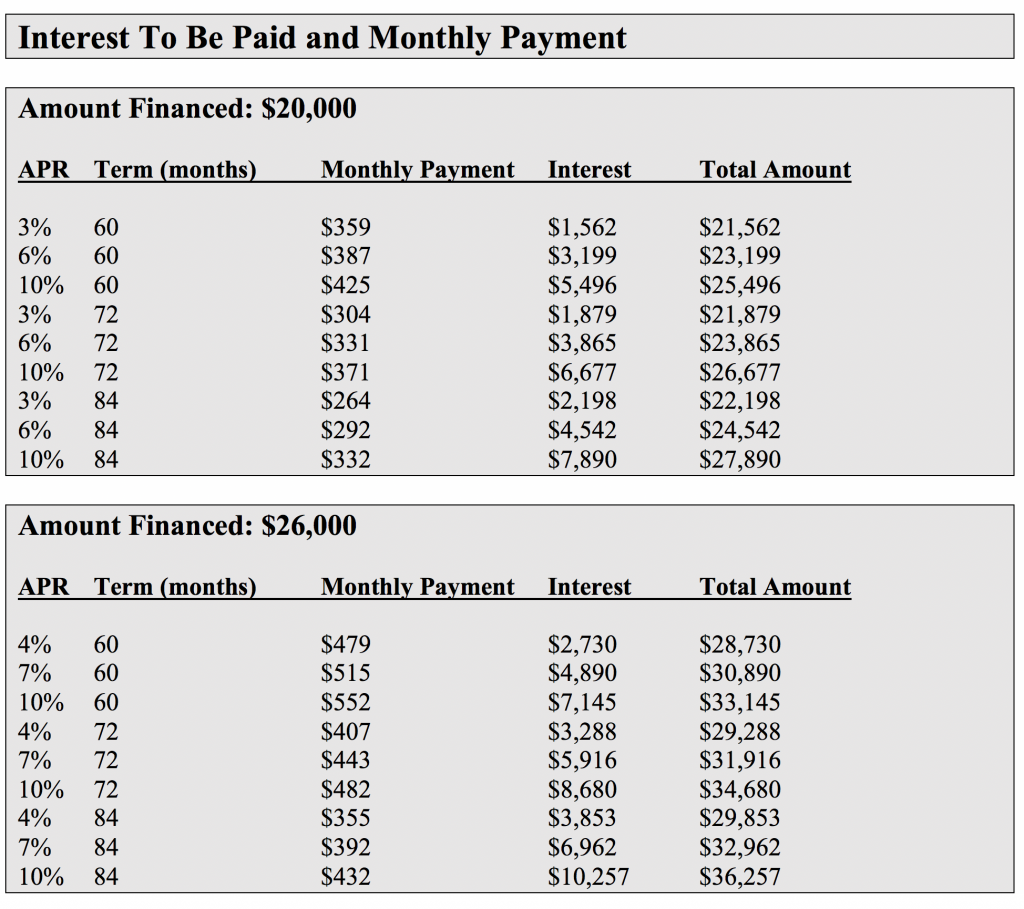

Example: Impact of Loan Terms on Monthly Payments

The chart below shows what happens to monthly payments and the total amount paid when the APR, amount financed, or loan duration changes. Let’s consider a car priced at $26,000, with a $6,000 down payment (including trade-in value). Subtraction makes the amount to finance $20,000. As the top line reveals, with a five-year term and tempting 3 percent APR, you’d be paying a total of $21,562 (including $1,562 in interest), at $359 per month. Raising APR to 6 percent raises the monthly payment to $387, and the total to $23,199. A weak credit record might raise APR to 10 percent, boosting the monthly outlay to $425.

Should I Buy a Car or Crossover?

How and Where To Get Financed

Bank, credit union, captive, finance company. Those are the four primary possibilities. Or, you can obtain credit directly from the dealership (typically at a higher interest rate).

Banks get a 29-percent share of new-auto financing, according to Melinda Zabritski at Experian, while finance companies account for 14 percent and credit unions make 17 percent of the loans.

Working directly with the dealership doesn’t mean you will be sending payments there. Dealers typically sell their loan contracts to a bank or finance company, which collects the monthly payments.

Traditional financing sources still operate from physical locations, but the internet is packed with online alternatives. Many are quite easy to use, even for those of us who aren’t wholly computer-literate. Most promise better rates, which may or may not be true. Still, some shoppers feel more comfortable dealing in-person with real people.

Should I Buy A Car From JD Byrider?

Special Finance

Special Finance

Though less common lately, car dealers have occasionally offered special low-interest programs to attract customers. Most are sponsored by auto manufacturers. Such special offers might be limited to certain models, or require specific loan details, such as a shorter-than-usual term. They may be available only to shoppers with high credit scores, or only to recent college graduates.

Speed-up Is Today’s Trend In Financing

Online car-buying services emphasize their speedy purchasing process. So do online financing sources, promising decisions in a matter of minutes. As one financing executive put it, any dealer failing to make a loan offer within, say, 15 minutes, will soon be an “also-ran.”

With automated online financing, “no staff interaction is required,” said Susan Perlmutter of Repay Holdings, at the 2021 Auto Intel Summit. “No sitting in front of a finance manager to see what you can and cannot afford.”

Do You Need a Co-signer?

Especially if your credit history is shaky, minimal, or short in duration, a loan grantor might insist that you obtain a co-signer for the auto loan. Be careful, though. If you fail to make payments at some point, that co-signer is liable for the balance of the loan. Make sure the co-signer understands what he or she is getting into before signing on the dotted line.

If you’re turned down for a loan, offering a bigger down payment would reduce the amount to be financed; but that might not be enough to convince an F&I person, or to improve your standing at a digital financing source. There are no quick “tricks” to boost that triple-digit FICO figure. All you can do is shop around, seeking a financing source that’s a bit more lenient. At least, with online financing, obtaining quotes from various sources is a lot easier than in the past.

Who Holds Your Contract?

Who Holds Your Contract?

Some years ago, while attending a conference on subprime financing, I was startled to learn that original issuers of loan contracts seldom kept them. Bundling contracts into groups and selling the whole batch to another organization was already a common practice. But securitization was fast becoming the norm. Going a step further, those groups were being traded in a marketplace similar to the stock market – a practice called securitization. Make sure you know the identity of the current holder, and who to contact with any problems.

Before you finance that new or used car …

- Determine how much you can afford – both the monthly payment and the total amount to be paid over the loan term.

- Finance a car only when you can afford to add a new payment to your monthly outlay.

- If affordability is an issue, consider delaying the purchase until you can amass a bigger down payment … or choose a cheaper model.

- Remember, what counts is the total amount you’ll be paying over a several-year term, not just the size of each monthly payment.

- Sign nothing until you’re sure you understand exactly what you’re agreeing to. You need specific answers, not ambiguous verbiage. Do you feel fully able to make those monthly payments through the number of months specified in the contract?

- Get a fully signed copy of the loan contract, whether it’s paper or digital. Make sure it has no blank spaces.

- Don’t forget that the total amount you’re paying may include sales tax (if applicable in your city and state) and, possibly, one or more fees.

Whatever type of loan you wind up with, you’re far from alone. Outstanding car loans in the U.S. have increased strongly of late, now approaching $1.3 trillion.

Information Sources

Credit Bureaus:

- Experian: 888-397-3742

- Equifax: 800-685-1111

- TransUnion: 800-916-8800

Several other online organizations can provide a free report on your credit score.

If you spot an error on your credit report, contact one of the credit bureaus immediately. Making a correction can spell the difference between obtaining a loan and being turned down.

Listen to the very entertaining Car Stuff Podcast

How to Finance Your Car